Integrated Wealth Management for modern financial lives.

Growth, income, cash flow, and major assets should work from one plan. We help investors, founders, families, and business owners coordinate decisions with a human fiduciary accountable for the advice.

Start with outcomes

What are you trying to do with your wealth?

The portfolio matters, but it is not the whole picture. A modern planning process starts with the financial life the portfolio is meant to support.

Build a portfolio with discipline around risk, time horizon, taxes, concentration, and liquidity.

Know what money is for before investing it: spending, reserves, taxes, business needs, and future opportunities.

Coordinate portfolio income, cash reserves, retirement timing, real estate, business interests, and distribution decisions.

See public markets, private investments, real estate, business value, and digital assets where relevant in one view.

AI and analytics can support research and documentation while human fiduciaries remain accountable.

Your financial life, mapped

More than an investment account

Income, cash reserves, growth portfolios, business value, real estate, private assets, family goals, taxes, estate documents, insurance review, and digital assets where relevant all shape the same set of decisions.

Our job is to help organize those moving parts into a process you can review, update, and act on with a human fiduciary accountable for client-facing advice.

See the planning processYour Financial Life

Career Income

Business Value

Tax Coordination

Digital Assets

Estate Coordination

Insurance Review

Growth Portfolio

Real Estate

Private Assets

Family Goals

Cash Reserves

Not a model-portfolio-only relationship

Built for wealth that cannot simply be moved into one account

Many advisory models begin with a transfer request: move everything to our custodian. That can be impractical when a meaningful share of your wealth is already committed to SPVs, venture funds, private-company equity, entity assets, digital assets, or positions you intentionally control elsewhere.

Protocol Wealth can advise around assets under advisement that remain outside our direct management or custody. The work is still specific: we take a view, model tradeoffs, and document advice under an advisory agreement rather than handing you generic best practices.

- Tax-aware coordination across public and private holdings

- Liquidity-event planning for SPV distributions, fund exits, and business proceeds

- Estate coordination for private assets and digital assets

- Cash-flow planning around illiquid venture investments and capital calls

- Concentration-risk review across public, private, and digital exposures

- Decision support for when not to invest in the next deal

- How much of your net worth is tied up in illiquid venture or private-company exposure?

- What capital calls, fund commitments, or liquidity events do you expect over the next five years?

- Are you overexposed to consumer crypto, infrastructure, AI, one employer, or another sector?

- How should your public-market portfolio offset your private portfolio?

- What happens if venture exits, token liquidity, or business proceeds take longer than expected?

Who we serve

When wealth gets more complex

Complexity can come from concentration, liquidity events, a business, a family balance sheet, an entity treasury, digital assets, or several of those at once. The point is not the label. The point is that the decisions are connected and need one accountable process.

View all audiencesWhat we solve

Knowing what money is for before investing it

Growth, income, reserves, operating cash, taxes, family needs, and future opportunities compete for the same capital. We help clients decide what to invest, what to keep liquid, what to reduce, and how each decision fits the broader plan.

How Protocol works

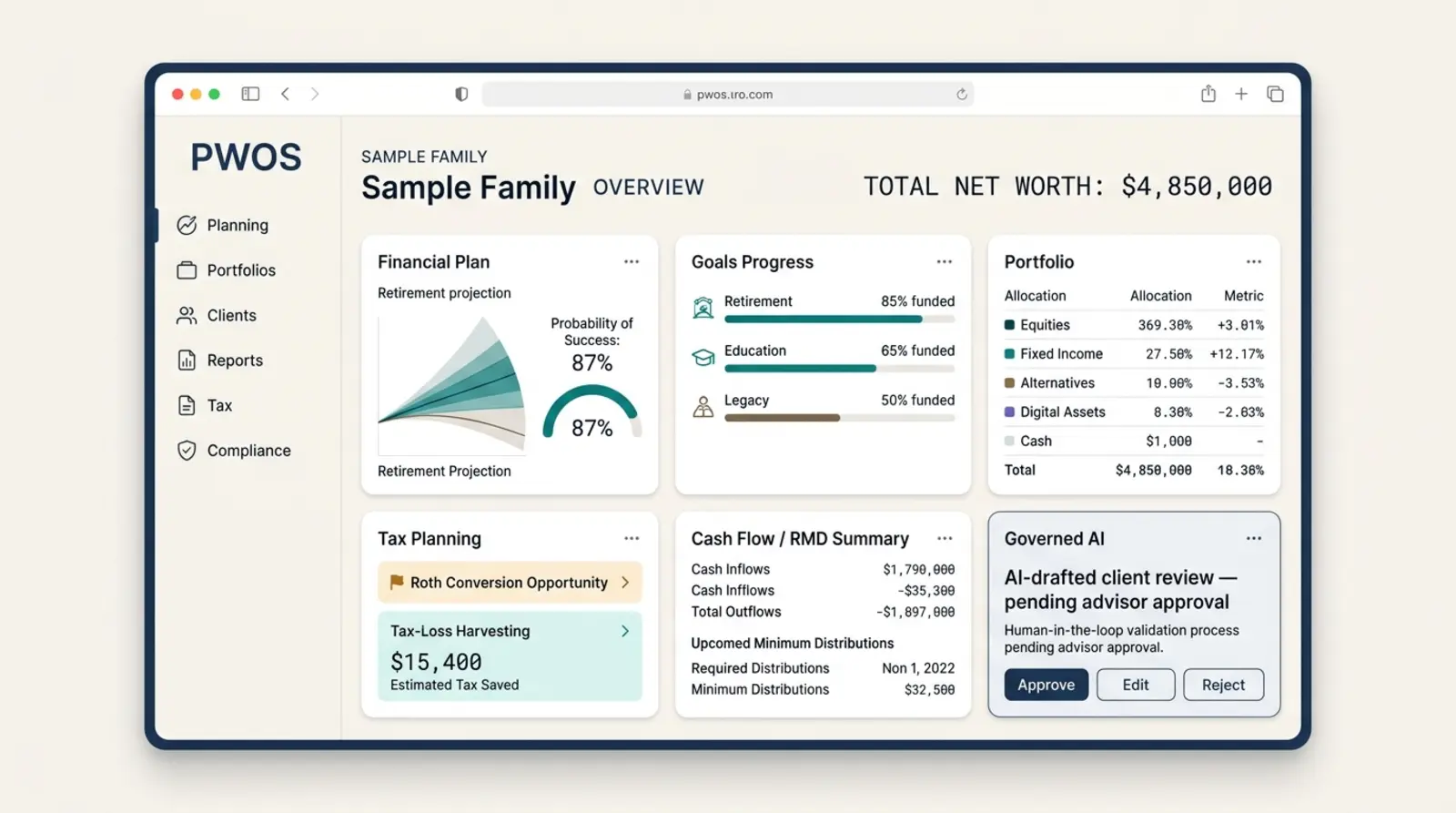

One fiduciary process, recorded end to end

Planning, portfolio, tax coordination, custody review, and treasury policy run through Protocol Wealth's operating system (PWOS). The technology is the proof layer: analysis stays consistent, every step is recorded, and a human fiduciary reviews client-facing recommendations.

Diagnostics

Start by mapping your financial life

The diagnostic hub helps you choose a path for growth, income, cash flow, concentration, liquidity, family wealth, entity treasury, and digital assets where relevant.

Systematic process

A modern planning process, not generic advice

Your financial life is too important for generic advice and too personal for black-box automation. Our process is designed to organize the facts, model tradeoffs, coordinate specialists, and keep a human fiduciary accountable for client-facing advice.

- 01

Map

Gain clarity

Organize assets, income, goals, obligations, values, and constraints.

- 02

Define

Set objectives

Clarify what growth, income, flexibility, family, and opportunity should support.

- 03

Model

Compare tradeoffs

Evaluate scenarios without turning estimates into promises.

- 04

Coordinate

Align resources

Work with CPAs, attorneys, insurance professionals, and other specialists where appropriate.

- 05

Implement

Act deliberately

Prioritize the next decisions and document the reason for each step.

- 06

Review

Adapt over time

Monitor progress and update the plan as markets, taxes, business needs, and life change.

Human fiduciary accountability

Technology supports research, organization, and documentation. It does not make autonomous client recommendations, execute trades, control assets, or replace fiduciary judgment.

Honest Fit

As fiduciaries, our obligation is to meet your goals — not impose our biases. We're both traditional and forward-leaning, which isn't for everybody. If we're not the right fit, we'll say so.

Want a systematic, research-backed approach applied to all asset types, traditional and digital

Have concentrated stock, private business value, SPVs, venture funds, entity cash, trust complexity, or token positions that need structured decisions

Need advice around assets that may remain with outside custodians, self-custodial platforms, funds, or other client-controlled positions

Want an advisor to take a specific view on your situation, not recite generic best practices

Value transparency — our process is documented, our profiles are public, and parts of the proof layer are open source

Are comfortable with a younger firm (formed 2025) that uses quantitative frameworks and technology under human fiduciary review

Conservative, passive wealth management? These fiduciary-only directories connect you with excellent advisors: XYPN, NAPFA, Let's Make a Plan.

Manage your own portfolio? Bogleheads is an outstanding community for self-directed, evidence-based investing.

Want a second opinion first? Schedule a consultation — we'll be honest about whether we're the right fit.

Conservative means different things to different people — it's not as simple as selecting a box. We think everyone could benefit from understanding their own behavioral biases and investment approach, regardless of which adviser they choose.

The team

Built by Operators and Investors

Protocol Wealth is a newer firm structure, but it is not starting from scratch. The partner-led team combines fiduciary advice, RIA operations, investment management, buy-side trading, digital-asset, compliance, operations, and technology backgrounds. Public registration records are available through FINRA BrokerCheck and SEC IAPD where applicable.

FINRA/SEC-registered since May 2009 → MML Investors Services → Cambridge Investment Research Advisors → Chart Wealth Management RIA → Interaxis founder (2019) + PlannerDAO co-founder → Protocol Wealth CCO (2025 – present)

LinkedIn

FINRA-registered since February 2000 → Morgan Stanley → Crabel Capital systematic futures desks (buy-side, 2003 – 2009) → Robert W. Baird → Fintrust → IMST Distributors → Fidelity Personal & Workplace Advisors → Protocol Wealth CIO (2025 – present)

LinkedIn

FINRA-registered since December 2011 → Navy SWO (USS Porter DDG-78) → Deloitte (PKI identity) → Merrill Lynch VP/Senior Financial Advisor (Oct 2011 – Jul 2022) → founded Ironclad Financial RIA (Jul 2022) → Protocol Wealth (2025 – present)

LinkedInClient assets are held with independent custodians or in client-controlled wallet infrastructure where appropriate. Protocol Wealth advises, monitors, and documents the process, but does not act as custodian and does not receive client private keys.

Custody & control

How assets are held

Client assets are held with independent custodians or in client-controlled wallets. Protocol Wealth advises, monitors, and documents the process, but does not take custody of client assets.

Where qualified custody is appropriate, assets are held with independent custodians. The custodian holds the assets; Protocol Wealth advises.

Where a client-controlled wallet is the better fit, permissions are documented, limited, and client-approved. We do not receive client private keys.

Technology helps us research, monitor, document, and review. Human fiduciaries remain responsible for advice, judgment, and client decisions.

Technology that proves the process

PWOS, PWAF, PWPortal, governed AI workflows, and open-source primitives support the advisory process. They are proof of consistency and auditability, not a replacement for human fiduciary judgment.

Defensive Patents

Three provisional patents filed defensively, so the patterns stay usable by every firm in the open-source community. Licensed under Apache 2.0.

Open source

Core compliance infrastructure is Apache 2.0 licensed. PII scanning, audit trails, and the safety layer that decides which AI tools are allowed to run, in what order, and with what approvals — available for any independent advisor to inspect, deploy, and build on.

Why open source?

Regulators should be able to inspect how AI handles client data. Advisors should own their tools, not rent them from vendors who change terms or sunset products on someone else's schedule. We publish primitives so the process can be inspected, while Protocol Wealth remains the fiduciary advisory firm accountable to its own clients.

Next step

Bring the full picture to one process

Schedule a consultation to discuss your current structure, what decisions are pending, and whether Protocol Wealth is the right fiduciary partner.

Protocol Wealth, LLC is an SEC-registered investment adviser (CRD #335298). Advisory services are provided only under a signed advisory agreement. See Disclosures, Form ADV, and Form CRS. All investing involves risk, including the possible loss of principal.